(And Why Knowing Them Can Make Borrowing Less Stressful)

Are you dreaming of a new car, planning for your child’s education, or finally buying the home you’ve been picturing for years? If so, chances are you’ll need financing at some point, and knowing what lenders look for can make the entire process feel a lot less intimidating.

Here’s the good news: loan decisions aren’t a mystery.

Whether you’re working with CCFCU or another financial institution, most lenders use the same basic framework to evaluate loan applications. It’s called the 5 Cs of Credit and understanding it gives you a huge advantage before you ever fill out an application.

Think of the 5 Cs as the lens lenders use to understand your financial story—not just a pass/fail test. Let’s walk through each one so you know exactly what’s being considered and why it matters.

What Are the 5 Cs of Credit?

The 5 Cs of Credit are:

- Capacity

- Capital

- Character

- Collateral

- Conditions

Each “C” represents a different part of your financial picture. No single factor tells the whole story as lenders look at how these pieces work together.

1. Capacity: How Much Debt Can You Handle? (Debt-to-Income Ratio)

Capacity answers one big question: Can you reasonably afford this loan?

Lenders look at your income and your existing debts to see whether you have room in your budget for another payment. One of the most common tools used here is your Debt-to-Income (DTI) ratio.

DTI Formula: Annual Debt Payments ÷ Annual Income

Let’s look at an example (numbers always make this clearer):

Income

- Annual salary: $84,000

Monthly debt payments

- Mortgage: $1,500

- Auto loan: $450

- Student loan: $200

- Credit card minimum: $150

- Total monthly debt: $2,300

Annual debt payments:

$2,300 × 12 = $27,600

DTI calculation:

$27,600 ÷ $84,000 = 33%

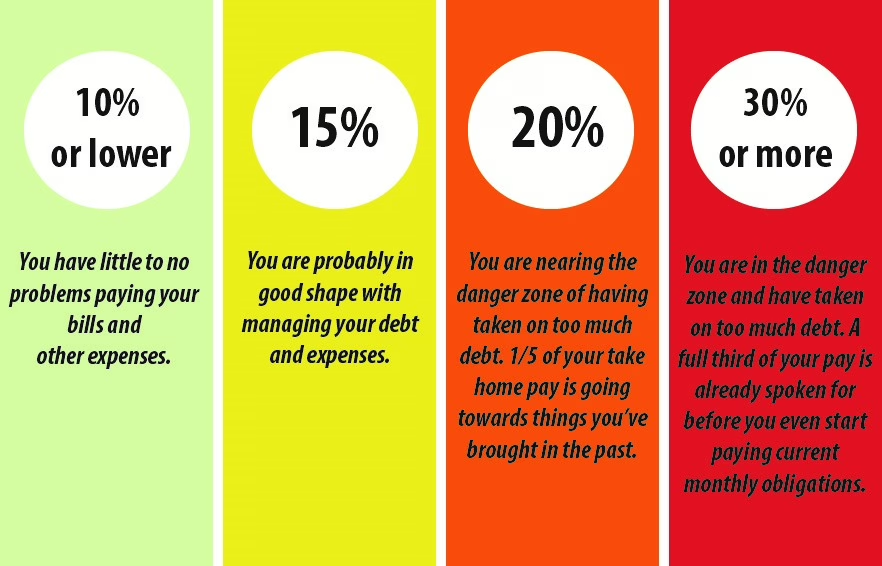

Lenders typically prefer a lower DTI as it shows you’re not stretched too thin. Here’s a quick visual guide to where your DTI might land:

Friendly reminder: A higher DTI doesn’t automatically mean “no.” It just means lenders need to look more closely at affordability.

At CCFCU we help members review their DTI and understand what it means with no judgment and no pressure, just clarity.

2. Capital: What Do You Have Set Aside? (Savings, Assets, and Down Payments)

Capital refers to the money and assets you already have available. This shows lenders that you’re financially prepared and invested in the loan.

Capital can include:

- Checking and savings balances

- Retirement accounts

- Investment accounts

- Other tangible assets

In many cases, capital shows up as a down payment. When you contribute your own money toward a purchase, it reduces the lender’s risk and shows commitment.

Think of it this way: when you’ve put your own skin in the game, lenders see that you’re more likely to protect that investment.

👉 Internal Link Opportunity:

Savings Accounts, Money Market Accounts, or “How to Save for a Down Payment”

3. Character: Your Credit History – (Trust and Accountability)

Character is where your credit report and credit score come into play. This is how lenders see how you’ve handled credit over time.

An easy way to think about your credit report is like a high school transcript. It doesn’t just show one test, it shows patterns. Just like a college can see your high school grades and whether you passed or failed algebra, lenders can see your history of payments, missed payments, or loans you’ve paid off successfully.

Lenders look at:

- Payment history

- Length of credit history

- Types of credit used

- Overall consistency

Missed payments happen. Life happens. What matters most is whether your history shows responsibility over time.

We’ll go much deeper into improving and rebuilding credit in Blog 3, so this post keeps the focus on understanding—not fixing.

4. Collateral: What Secures the Loan? – (Something of Value)

Collateral is an asset you agree to use as security for certain loans. It helps protect the lender if the loan isn’t repaid.

Common examples include:

- Vehicles (auto loans)

- Real estate (mortgages or home equity loans)

- Investment accounts

- Equipment (for business loans)

For example, with an auto loan, the vehicle itself usually serves as collateral. If payments stop, the lender may repossess the vehicle. And yes, this is the part no one loves to think about, but it’s important to understand how secured loans work.

We’ll talk much more about auto loans and home-related lending in later blogs in this series.

5. Conditions: What’s Your Story? – (Context Matters)

Conditions refer to outside factors or life events that may have impacted your finances or credit.

This can include:

- Job loss or income changes

- Medical emergencies

- Divorce

- Identity theft

- Economic Factors

Lenders know numbers don’t tell the whole story. Being prepared to explain past challenges and how you have been resilient through those challenges can make a real difference.

Pro Tip: If you ever think you might miss a payment, reach out to your lender early. At CCFCU we like to focus on upfront communication and solutions, not penalties.

Why the 5 Cs Matter (And Why This Helps You)

Understanding the 5 Cs of Credit puts you in the driver’s seat. Instead of wondering why a decision was made, you understand the factors behind it.

At CCFCU, we look at the full financial picture because lending should feel personal, especially here in West Texas where relationships still matter.

What’s Next in the Series?

Now that you understand the framework lenders use, the next step is learning how these factors come together during an actual loan decision.

Up Next:

How to Get Approved for a Loan: What Lenders Look For

Have questions about your credit, your options, or where you stand today? You don’t have to figure it out alone.

The lending team at CCFCU is here to help you understand the process and move forward with confidence.